Risk-free discount rate assumptions

Promoting consistency in risk-free discounting for technical provisions

Constructing assumptions for forward risk-free rates of discount is core to actuarial work.

The Australian Accounting Standards Board requires that provisions for general insurance liabilities should include an allowance for inflation and are discounted at the risk-free rate.

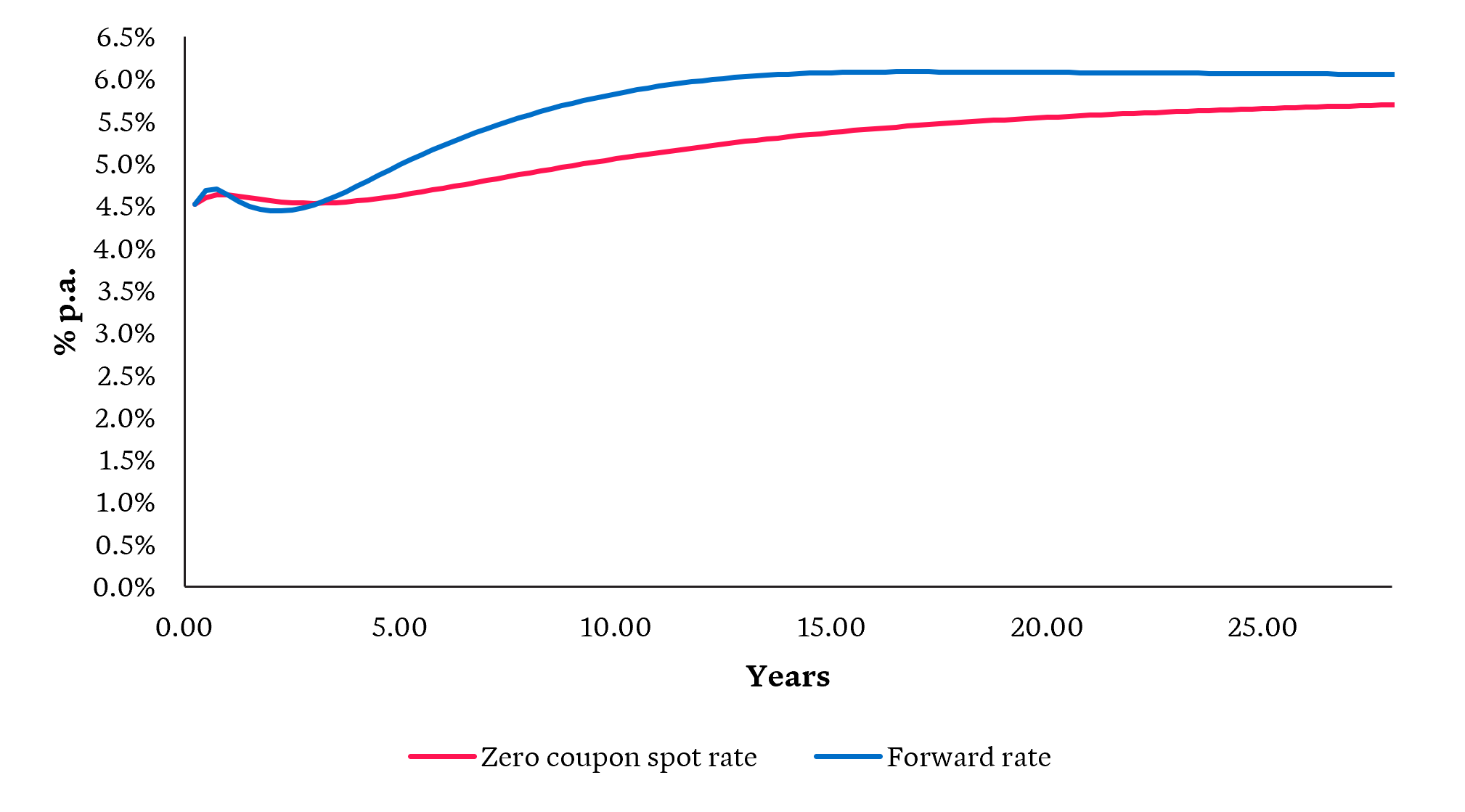

Taylor Fry will publish our Australian risk-free discount rate assumptions (yield curve) monthly to promote consistency in the application of risk-free discounting for technical provisions across Australia. Our team derives assumptions for an implied forward rate curve using publicly available Commonwealth Bond pricing, insights gained from our own research and in-depth market experience.

In developing our assumptions, our approach aims to deliver a set of forward rates with the following characteristics:

- Smooth – Parsimony is an important principle in yield curves

- Fits observable bond prices well – A good fit means that the price of those cash flows based on the forward rates is close to the observed bond price

- Exhibits reversion over the long term – The model should be able to impose reversion to the long-term rate at terms beyond observable bond prices.

Our combined approach to inflation and discount rate assumption-setting is set out in Hugh Miller and Tim Yip’s paper in the Australian Journal of Actuarial Practice Volume 5 2017.

The yield curve will be published on the first week of each month.

Taylor Fry’s Australian

risk-free discount rate assumptions

Based on Commonwealth Bond Pricing as of 29 July 2026.

Risk-free rates previous releases (2026)

While we’ve prepared these discount rate assumptions with due care:

- Third parties shouldn’t place any reliance on this work that would result in any duty or liability to Taylor Fry

- Taylor Fry won’t be liable for any damage or losses incurred by any party as a result of having received, acted on, or relied on this work.

Using our discount rate assumptions will be an automatic acceptance of these conditions.

Risk-free rates releases archive (2025 and older)

Our leaders in

Risk-free discount rate assumptions

Our leaders in Risk-free discount rate assumptions

Recent insights

Recent insights

More articles

APRA’s latest NCPD data points to an uneven liability market

Our initial analysis of APRA’s latest NCPD data points to five key movements insurers, brokers and insureds should be watching.

Read Article

Behind the headline – What May’s CPI data means for insurers and Australia’s insurance market

The latest CPI data reveals three pressure points insurers should be watching now.

Read Article